Yahoo Lifestyle

Yahoo Lifestyle Our Take On Flexible Solutions International's (NYSEMKT:FSI) CEO Salary

Dan O’Brien has been the CEO of Flexible Solutions International Inc. (NYSEMKT:FSI) since 1998, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Flexible Solutions International.

Check out our latest analysis for Flexible Solutions International

How Does Total Compensation For Dan O’Brien Compare With Other Companies In The Industry?

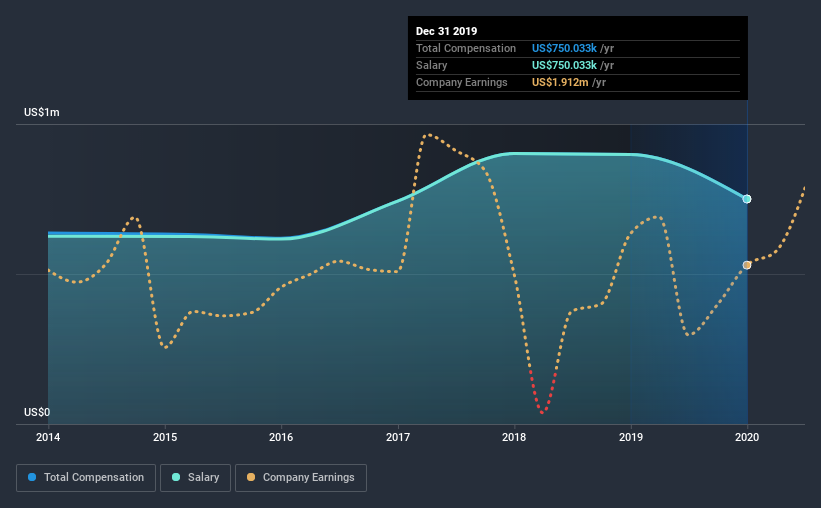

Our data indicates that Flexible Solutions International Inc. has a market capitalization of US$27m, and total annual CEO compensation was reported as US$750k for the year to December 2019. Notably, that's a decrease of 16% over the year before. It is worth noting that the CEO compensation consists entirely of the salary, worth US$750k.

In comparison with other companies in the industry with market capitalizations under US$200m, the reported median total CEO compensation was US$389k. Hence, we can conclude that Dan O’Brien is remunerated higher than the industry median. Furthermore, Dan O’Brien directly owns US$10m worth of shares in the company, implying that they are deeply invested in the company's success.

Component | 2019 | 2018 | Proportion (2019) |

Salary | US$750k | US$898k | 100% |

Other | - | - | - |

Total Compensation | US$750k | US$898k | 100% |

On an industry level, around 19% of total compensation represents salary and 81% is other remuneration. At the company level, Flexible Solutions International pays Dan O’Brien solely through a salary, preferring to go down a conventional route. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Flexible Solutions International Inc.'s Growth

Over the last three years, Flexible Solutions International Inc. has shrunk its earnings per share by 8.0% per year. In the last year, its revenue is up 14%.

The decline in EPS is a bit concerning. There's no doubt that the silver lining is that revenue is up. But it isn't sufficiently fast growth to overlook the fact that EPS has gone backwards over three years. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Flexible Solutions International Inc. Been A Good Investment?

Most shareholders would probably be pleased with Flexible Solutions International Inc. for providing a total return of 42% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

Flexible Solutions International rewards its CEO solely through a salary, ignoring non-salary benefits completely. As we touched on above, Flexible Solutions International Inc. is currently paying its CEO higher than the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. We feel that EPS have been a bit disappointing, but it's nice to see positive shareholder returns over the last three years. Considering positive investor returns, it would be bold of us to criticize CEO compensation, but shareholders might want to see healthier EPS growth before a raise is given out.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We've identified 2 warning signs for Flexible Solutions International that investors should be aware of in a dynamic business environment.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.